Thursday, 25 February 2010 16:12

EU interim forecast: recovery is in progress but remains fragile

Categorized as :

The EU economy is gradually recovering, whilst still facing headwinds. Real GDP started to grow again in the third quarter of 2009, ending the longest and deepest recession in the EU's history. The exceptional crisis measures put in place in the EU played a major role in turning the economy around. However, in line with the autumn 2009 forecast, growth eased in the fourth quarter, as the impact of some temporary factors started to fade. According to the current update, the economic outlook for the EU remains broadly unchanged. GDP is projected to grow at 0.7% in both the EU and the euro area in 2010. The inflation projections also remain largely unchanged at 1.4% and 1.1% in the EU and the euro area, respectively. Uncertainty surrounding these projections remains rife, as recent developments in financial markets illustrate well,

Commissioner for Economic and Monetary Affairs Olli Rehn said: "The recovery of the EU economy is materializing but it is still fragile. Putting the European economy back on a strong and sustainable path should be our overarching objective. For this we need to work on two fronts: the economic recovery and the consolidation of our public finances. The new Europe 2020 Strategy leading to the modernization of our economies should go hand in hand with the consolidation of our public finances. This is necessary for sustainable growth and job creation."

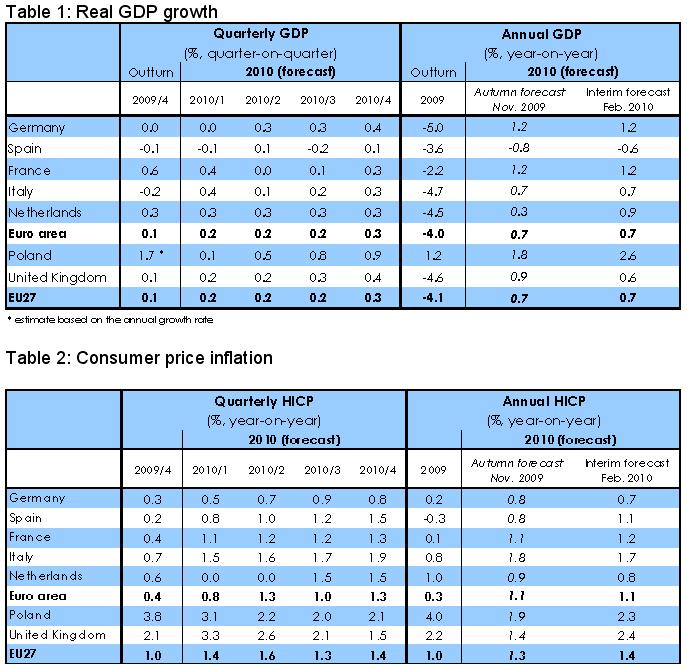

Growth forecast for the EU and the euro area on track

Growth projections for the first half of this year have been revised slightly upward in the Commission's forecast for both the EU and the euro area. But because of marginal downward revisions for the second half of 2010, the projected rate of GDP growth in 2010 as a whole remains broadly unchanged at 0.7% in both areas. This is calculated on the basis of updated projections for France, Germany, Italy, the Netherlands, Poland, Spain and the United Kingdom, which together account for about 80% of the EU's GDP.

Stronger global recovery

Global economic activity proved more robust in the second half of 2009 than previously expected, especially in emerging Asia. Real GDP (excluding the EU) escaped an outright fall last year and is now expected to grow by some 4¼% in 2010. Regarding the near term, global indicators are encouraging, partly reflecting the inventory cycle in manufacturing.

Further out, world growth is set to hit a soft patch, due to the gradually fading effect of the stimulus measures and because of the inventory cycle. Differences across countries remain sizeable, with a markedly more solid recovery for emerging economies, on the back of resuming capital inflows, and the return of investors' risk appetite. While the EU's external environment is recovering faster than expected, it remains to be seen to what extent this will help the EU this year.

Modest impact on domestic dynamics so far

Improved sentiment indicators for the EU point to an expansion of activity going forward, but hard data, especially industrial production and retail sales, have been less encouraging recently. While a better-than-expected external environment could spur exports further, investment remains very weak, reflecting exceptionally low capacity utilisation rates. Residential investment is also likely to be weak in 2010, given the required adjustment in housing sectors in several Member States. Financial-market conditions have recovered since early 2009, but balance-sheet adjustment is not complete and uncertainty remains abundant. A muted outlook for investment typically implies a weak labour market ahead, which in turn is likely to dampen private consumption. With many of the main driving forces being still temporary in the EU and globally, the robustness of the recovery is yet to be tested.

Price stability maintained

The strong disinflation process over most of 2009 was mainly explained by downward base effects from the energy and food components and by a growing slack in the economy. HICP inflation rose somewhat in the last months of 2009, and remained at a very moderate annual rate of 1.0% in the EU and 0.3% in the euro area, as expected in the autumn. Looking forward, a sizeable slack in the economy is set to keep inflation in check, offsetting increases in energy and commodity prices. Price stability is expected to be maintained, with HICP inflation projections being only marginally revised upwards to 1.4% in the EU and staying unchanged at 1.1% in the euro area.

Risk assessment

The risks to the EU growth outlook for 2010 still appear broadly balanced. On the downside, the situation of financial markets remains highly uncertain and subject to serious adverse risks. On the upside, the vigour of the global recovery, particularly in Asian emerging markets, and the imminent turning of the inventory cycle in the EU may have a greater impact on domestic demand than currently anticipated. As regards the inflation outlook, risks also appear to remain broadly balanced for 2010.

More information can be obtained by the EC Website for Economic and Financial Affairs

Back to "News - Announcements"

News categories

Περιοχή μελών - Εγγραφή στο Newsletter

Αν θέλετε να λαμβάνετε ενημέρωση από το enterprise europe network, εγγραφείτε στο newsletter